Capital One Credit Wise Review: Accurate? [2020]

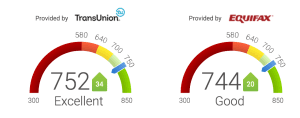

Keeping up with your credit score and report is crucial given all of the different ways that your credit score can impact your daily life. But it can be a

Keeping up with your credit score and report is crucial given all of the different ways that your credit score can impact your daily life. But it can be a

The cornerstone of award travel is your credit score. Without at least a decent credit score, you’re going to get hit with denials on your credit card applications left and right