American Express CID (CVV) Code Guide [2022]

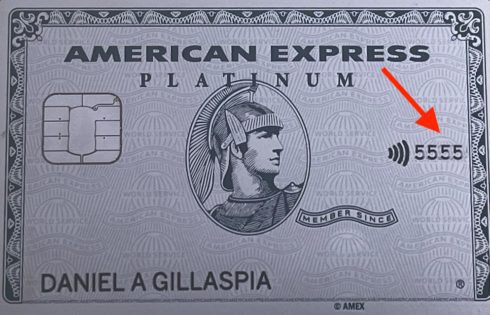

When it comes to finding your security code for your American Express card, things aren’t always so straightforward, especially if you are used to other cards like those from MasterCard

When it comes to finding your security code for your American Express card, things aren’t always so straightforward, especially if you are used to other cards like those from MasterCard

Capital One has some of the best credit cards out there. The only problem is that sometimes you are not given a credit limit big enough for your spending needs

At some point you might consider downgrading, product-changing, or cancelling your Chase Sapphire Preferred card. There are a number of factors that you want to consider before deciding which route

Getting an Amex credit limit increase is pretty straight forward. However, there are a few things you should know like how big of an increase you should request and how

Sometimes you get to a point where you just no longer need a credit card. In those instances, you might be very tempted to proceed with canceling your card. However,

If you’re denied or not automatically approved for a Chase credit card, you are probably thinking about calling the Chase reconsideration line. But before you ever give them a call,

Offers contained within this article maybe expired. In addition to expiration dates, some credit or debit cards may display how long you have been a member with their banking establishment.

One of the best perks of Chase credit cards is that you can often get a credit line increase for your credit cards. It’s generally a pretty straight-forward process but

Are you trying to check your Barclays credit card application status? Well, you’re in luck as Barclays makes it easy to check your status with a simple application status checker.

Requesting a credit line increase from Discover is a pretty easy task. The hard part is predicting what the outcome of your request will be, though. In this article, I’ll