Citi AAdvantage Globe Card Live (90,000-Mile Bonus)

Citi has launched a new American Airlines credit card designed for frequent flyers looking to boost their AAdvantage miles balance while gaining access to premium travel perks. With a 90,000-mile

Citi has launched a new American Airlines credit card designed for frequent flyers looking to boost their AAdvantage miles balance while gaining access to premium travel perks. With a 90,000-mile

Offers contained within this article maybe expired. The Platinum Card from American Express is the best credit card for lounge access, at least in my opinion. Many people only think

Advertiser Disclosure: UponArriving has partnered with affiliate partners and may receive a commission from card issuers. UponArriving does not display all credit card offers and affiliate relationships may impact how offers

Advertiser Disclosure: UponArriving has partnered with affiliate partners and may receive a commission from card issuers. UponArriving does not display all credit card offers and affiliate relationships may impact how offers

The Southwest Rapid Rewards® Priority Credit Card is loaded up with some interesting benefits like a travel credit, upgraded boardings, and right now it comes with a very solid limited-time

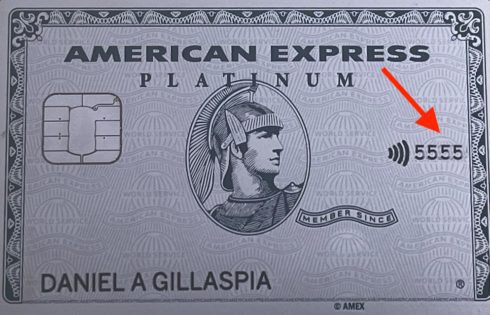

When it comes to finding your security code for your American Express card, things aren’t always so straightforward, especially if you are used to other cards like those from MasterCard

Capital One has some of the best credit cards out there. The only problem is that sometimes you are not given a credit limit big enough for your spending needs

At some point you might consider downgrading, product-changing, or cancelling your Chase Sapphire Preferred card. There are a number of factors that you want to consider before deciding which route

Getting an Amex credit limit increase is pretty straight forward. However, there are a few things you should know like how big of an increase you should request and how

Sometimes you get to a point where you just no longer need a credit card. In those instances, you might be very tempted to proceed with canceling your card. However,