[Offers contained within this article may no longer be available]

A lot of people seem to ask which AMEX card is best for them: The American Express Platinum or the Premier Rewards Gold Card (PRG). Both are great cards that I enjoy using but for very different purposes. This article will show you the important differences between the cards that will make your decision easier when applying for these cards. Ultimately, you will see that the Platinum is all about the travel benefits while the PRG is all about earning Membership Rewards (and a little about the benefits).

Both are charge cards

First, don’t forget that both of these two cards are “charge cards.”

A charge card must be paid off in full each month or else you face a hefty monthly fee. Sometimes, after you’ve used a charge card for about a year, Amex will then offer you the option of carrying a balance (this usually comes with a MR bonus as well). However, you cannot initially carry a balance on a charge card like you can on a credit card.

Transfer Partners

Both cards earn Membership Rewards that transfer to travel partners. There’s no difference here but just for a refresher, here are the transfer partners of Membership Rewards.

Airlines

- Delta Skymiles

- Club Premier AeroMexico

- Aeroplan Air Canada

- Flying Blue Air France/KLM

- MilleMigilia Club Alitalia

- ANA

- Asia Miles

- Avios British Airways

- Emirates Skyrewards

- Hawaiin Airlines

- Iberia Plus

- JetBlue

- KrisFlyer Singapore Airlines

- Virgin America

- Virgin Atlantic

Hotels

- Best Western Rewards

- Choice Privileges

- Hilton HHonors

- SPG (Starwood Preferred Guest)

Sign-up Bonus

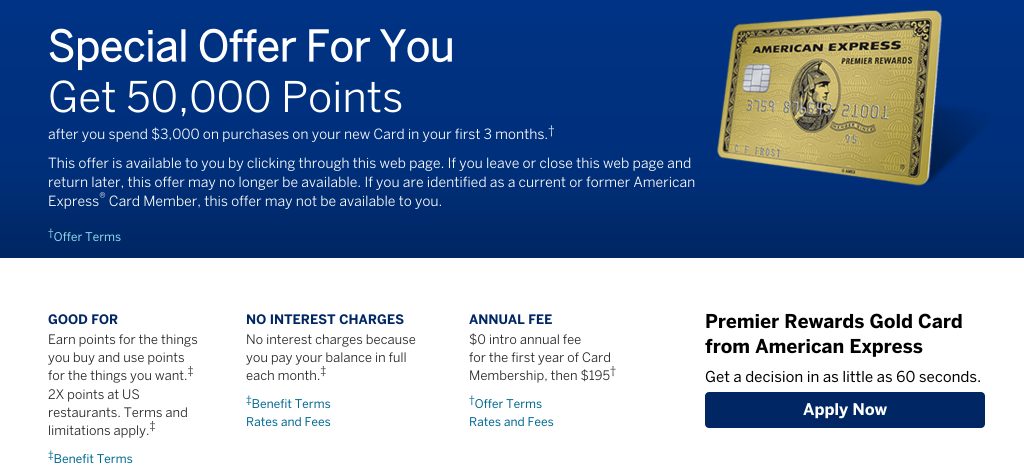

AMEX PRG

- 25K to 75K when you spend $1,000-$3,000 in the first 3 months

In my opinion you should hold out on the PRG until you can get the 50K offer. It’s different for everyone but pretty much every other time I check credit cards on the Amex website, I am invited to apply for the “special offer” of 50,000 points. Some people hold out for the 75K offer but that is known to be an extremely rare offer that could leave you waiting months and months and possibly even years to see (if ever).

AMEX Platinum

- 40K to 100K when you spend $3,000 in the first 3 months.

The 40K offer is the standard offer available to the public. The 100K offer comes around in three forms and there’s no guarantee that you will ever get it. The three forms it comes in are:

- 1) Targeted mailings (if you’re already an Amex cardholder your chances of getting this offer in the mail are slim to none).

- 2) Pre-approval links: Some sites (including the Amex site) that allow you to view your pre-approved credit card offers will show this offer.

- 3) Incongnito/Private browser windows sometimes show this offer (rare)

Tip: When applying for bonuses with Amex cards always remember that bonuses for personal cards are only given once a lifetime (although not 100% enforced). The main exception I see with this are reports of others being approved for the same card a second time and receiving the difference between their first bonus and the later bonus. For example, if you applied for the Platinum for the 40K offer your first go around and the 100K offer for your second, Amex would grant you a total of 60K additional points for your second bonus.

Bonus Points Potential

The PRG puts the Platinum to shame in terms of bonus earning potential.

AMEX PRG

- 3X on Airline Tickets (4X through the Amex Portal)

- 2X on Dining

- 2X Groceries

- 2X Gas

- 1X on all other purchases

AMEX Platinum

- 1X on all purchases (*crickets*, I know)

This is the first key difference between the cards: the Premier Rewards Card is primarily for earning points to transfer to travel partners. In my opinion, it is one of the best earning travel cards along with the Chase Sapphire Preferred and the Citi Thankyou Premier.

A quick aside: If you are highly concerned with earning a lot of MRs through bonus category spending I would definitely consider the Amex Everyday Preferred. Under the average consumer’s spending habits, more points can be earned with this card than the PRG.

Benefits

AMEX PRG

Outside of the $100 airline statement credit and no foreign transaction fees, there aren’t really any more benefits that come with the PRG.

AMEX Platinum

Benefits is where the Platinum really proves its worth.

Here’s a breakdown of my favorite benefits of the Platinum, but in a nutshell this card confers a host of benefits to you making it worth it including:

- Priority Pass airport lounge access (worth $400 per year)

- Centurion Lounge Access

- $200 annual airline credit (essentially reducing the annual fee to $250)

- $100 statement credit for Global Entry/TSA Pre-Check (a Godsend that’s good for 5 years!)

- Add up to 3 authorized users for only $175 per year (for all 3)

- Gold status with Hilton and Starwood

- Free Boingo Wifi subscription (worth $120 per year)

- Rental car benefits like express check-in, free upgrades, and discounts

These benefits easily pay for the value of the card and much, much more when considered in conjunction with the sign-up bonus.

However, the key question is whether the benefits are useful to you. Answering this question is the simplest way to decide if you even wan’t anything to do with the Platinum.

If you only travel about 2 times a year domestically and don’t really care for lounge access or other perks like hotel status, the Platinum is really only useful to you for the sign-up bonus (and in that case maybe you want to wait around for the 100K offer). On the other hand, if you travel frequently (especially internationally) and/or highly value comfort and convenience when you travel then the Platinum is definitely worth to consider.

If you fall somewhere in between then it’s a little less clear-cut for you. If you find yourself in this group don’t knock the benefits without trying them. For example, if you’ve never spent time in an airport lounge you could always pay for a day pass to a lounge like the Centurion or similar and see if that’s something you’d value having access to each time you visit the airport. I think a lot of people will realize if the “lounge life” is worth it to them after just a visit or two and will be able to more accurately gauge how much they really value lounge access.

No Foreign Transaction Fees

Both cards have no foreign transaction fees.

Annual Fee

AMEX PRG

- $195, waived the first year (more like $95/year with airline credit)

AMEX Platinum

- $450, not waived (more like $250/year with airline credit)

A lot of people have an instant “yikes” reaction to annual fees like this and almost immediately discount the card. But don’t do that because the Platinum can be worth so much more than $450 (and as you’ll see the annual fee is more like $250 per year).

You can read about getting the Priority Pass with the Amex Platinum here, where I talk about why I think the benefits of the Platinum more than pay for themselves. The Platinum is not for everybody but for many people, the $450 is more than worth it for this card.

Downgrading

Because these are both charge cards you can only “downgrade” or “product change” them to other Amex charge cards without incurring a hardpull. Unfortunately, there’s really no charge cards that are worth to downgrade to. You can read some about the Green Card and the standard Gold Card in my article, Which American Express Card is best for you?, but you’ll see that’s it’s not worth it to product change to those cards if you’re still interested in earning significant rewards.

If you ever decide to cancel the Platinum or the PRG then I recommend applying for the Amex Everyday if you are still carrying a balance of MRs. It has no annual fee and earns a decent amount of points via bonus spending, but most importantly, it will preserve your MRs while you decide how to best use them.

Tip: Don’t let the customer service reps from Amex confuse you by using the term “product change” — if you change from a charge card to a credit card there will almost always be a hard pull on your credit regardless of how the rep “phrases” it.

The Verdict

As is often the case the answer to this is “it depends.” Again, it’s all about whether your goals are to earn the most MRs or to obtain all of the travel benefits and/or a hefty sign-up bonus.

Don’t rule out applying for both of these cards, either. As already mentioned, it’s absolutely possible to be approved for both the Platinum and the PRG at the same time. That means that if you caught it at the right time you could earn 150-175K of MRs for spending about $4,000 in 3 months. An outstanding gain.

Tip: Keep it nice and slow when applying for Amex cards. If you quickly obtain 4 or more approvals within the span of a couple of months there’s a good possibility you might be financial reviewed. It’s not a death sentence by any means but it’s something that can often result in reduced credit limits (rarely closure) for those who misrepresented their income so it’s best avoided. So just pace yourself with these applications.

Daniel Gillaspia is the Founder of UponArriving.com and the credit card app, WalletFlo. He is a former attorney turned travel expert covering destinations along with TSA, airline, and hotel policies. Since 2014, his content has been featured in publications such as National Geographic, Smithsonian Magazine, and CNBC. Read my bio.