It looks like Citi might be in the process of making some big changes to some of its credit card application rules for its American Airlines cards. These new changes have some pros and cons but you definitely want to be up to date on these changes because they could alter your strategy for maximizing miles.

Table of Contents

The old (but still current) rules

A while back, Citi changed their application rules for the American Airlines credit cards. They decided to limit you to one AA sign-up bonus per 24 months. The language reads:

American Airlines AAdvantage® bonus miles are not available if you have had any Citi® / AAdvantage® card (other than a MileUp℠ or CitiBusiness® / AAdvantage® card) opened or closed in the past 24 months.

Practically what this meant is that if you picked up the Citi Platinum Select sign-up bonus you would not be able to get the bonus for the Citi Executive AA card until waiting 24 months. Moreover, if you closed your Citi Platinum Select (maybe to avoid the annual fee), that clock would be reset. So this made it difficult to score a lot of AA miles with Citi cards and forced some people to pay an annual fee they didn’t want to pay.

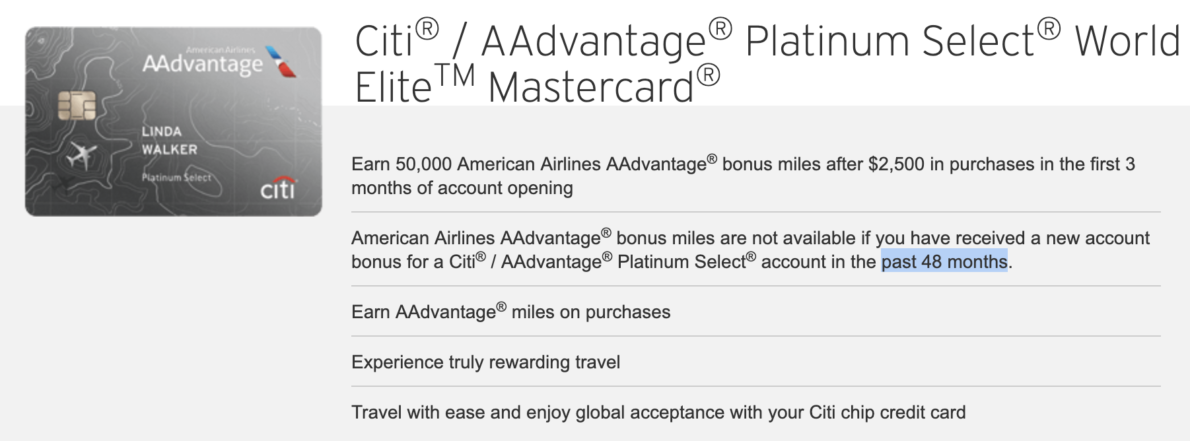

The new Citi AA rule

The new rule that is showing up on various links like this and changes the clock to 48 months.That sounds horrible but it also removed the “family restriction” and the language about closing cards. Here’s what the rule looks like:

American Airlines AAdvantage bonus miles are not available if you have received a new account bonus for a Citi / AAdvantage Platinum Select account in the past 48 months.

This means that you will have to wait 48 months between bonuses but you should be able to pick up multiple AA cards around the same time (or stagger them). Either way, you shouldn’t be limited to one Citi AA card bonus per 48 months. And since the language about closing cards is absent, you won’t have to worry about paying annual fees just to keep your card open.

So for some people who just need to haul in AA sign-up bonuses for up-front value, this rule could help them since they will probably be able to pick up two cards at around the same time.

If you’ve received your last Citi AA bonus over two years ago (but not longer than four years) from a card like the Platinum Select, then you might want to jump on the Platinum Select before this rule goes into effect. That’s because if the new rule came into effect overnight, you could find yourself ineligible for a while.

The current offer is for 60,000 miles after spending $3,000 in purchases in the first 3 months of account opening. That’s not an affiliate link and I receive no commission for that offer — just trying to look out for ya!

If you were recently approved for the Platinum Select, it’s possible that with the new rules you could apply for the Citi Executive (link with 48 month language) and get a second AA bonus (if you haven’t gotten the Executive bonus in 48 months). You’d then be out of luck for those cards for up to four years but at least you’d have points now. And with the AA dynamic awards looming, that wouldn’t be a bad strategy.

But again, this is still semi-speculation we’re talking about and we don’t know exactly how this will all play out, so proceed with that in mind.

The work-around: targeted mailers

It is possible to receive targeted mailers that will allow you to get around these rules. It’s not clear how these mailers will be affected by these new rules and what that might look like. But my advice would be to jump on these ASAP if you receive them because they could become a thing of the past at some point in the near future.

Final word

This would be another instance of banks changing up the rules to prevent rewards abuse but it’s not that 100% negative for folks who will be looking to hit up a couple of AA cards around the same time since it opens up more short-term opportunities.

It’s important to note that we still don’t know if these rules will be implemented officially across all Citi AA credit card application pages. Right now they are not and they might not be adopted fully. But in the event that they are, you deserve a heads up about the changes.

H/T: DD

Daniel Gillaspia is the Founder of UponArriving.com and the credit card app, WalletFlo. He is a former attorney turned travel expert covering destinations along with TSA, airline, and hotel policies. Since 2014, his content has been featured in publications such as National Geographic, Smithsonian Magazine, and CNBC. Read my bio.

I was approved for the AS Platinum earlier this year; are you saying that I could get a signup bonus now if I’m approved for the Executive AA? Also, could I get the bonus for the Business AA as well?

Thanks,

Rod

When you say AS, do you mean AA Platinum Select? If so then it’s possible you could get the bonus for the Executive based on the language found on the application page linked in the article but we still don’t know 100% how that will play out. But when it comes to the business, yes you can get that in addition to the personal. 👍

Thank you! Yes, I meant AA not AS; sorry for the typo. I am hoping to pull the trigger on the Business card in August; I guess the Executive is out of the picture for me at the moment as I’m working to get under Chase 5/24. Thanks again!

No prob. And yeah I would def wait on the Exec if you’re trying to get down under 5/24!

Hi Daniel,

I’m trying to get under Chase 5/24; the only business card I currently have is the Amex Bonvoy Business card. In the meanwhile, what other business cards can I apply for?

Thank you!

You can apply for just about any of the major issuers except for Capital One and Discover. So I’d think about Amex, Bank of America, and Citi biz cards.

Hi Daniel,

Could u pls recap the chase 5/24 rule? Tnxx

Great; thank you!