Have you ever paid for an item or service with your credit card only to be severely disappointed with the quality of the product or service? Or have you ever found questionable charges on your credit card statement?

In this article, I will discuss the process for how to handle a disputed charge with Chase. I’ll go into some details that you should consider before disputing a charge and also discuss the process of initiating a disputed charge with Chase.

Table of Contents

How to dispute a Chase credit card charge

You can dispute a Chase charge in a few ways: online, by mail, fax, or even over the phone.

Online

To file a dispute online, simply log-in to your account and follow the steps below.

You can send in your dispute to the following address:

Customer Service

P.O. Box 15299

Wilmington, DE 19850-5299

Fax

Fax to: 1-888-643-9624 Attn: Cardmember Services – Dispute Resolution

Phone

To initiate a claim over the phone just call the phone number on the back of your card Monday through Friday from 7 AM to 10 PM Eastern time, and Saturday and Sunday from 9 AM to 8 PM Eastern time.

Note that this article will focus on personal Chase cards, such as the Chase Sapphire Preferred, Chase Sapphire Reserve, and other Chase co-branded credit cards. If you’re dealing with a small business credit card such as the Chase Ink Business Preferred, I suggest calling the number on the back of your credit card.

Tip: Use WalletFlo for all your credit card needs. It’s free and will help you optimize your rewards and savings!

Before disputing a charge

Before you ever contact Chase to initiate the dispute process, you should try to contact the merchant directly and resolve the issue.

Why you should contact the merchant

One of the major reasons why you want to try to resolve the issue with the merchant directly is because it just makes things easier for everybody involved.

Merchants get penalized when they are hit the chargebacks and have to pay fees and hassle with a lot of paperwork. Getting hit with chargebacks can also cause issues with the merchant’s relationship with the credit card issuers. Thus, most merchants usually have a strong incentive to avoid chargebacks.

Processing chargebacks can also be very time-consuming for the consumer. It can mean rounding up supporting documentation and waiting several weeks to even months for resolution. It can also mean unwanted eyes on your accounts. So it can be a better use of your time to just try to resolve things directly with the merchant.

How to resolve things with merchants

You can attempt to resolve chargebacks in a variety of ways.

Phone call

The easiest way (in theory) would be to simply call up the merchant and try to work out a refund or a return or some other type of compensation that you would consider fair. You can often find their number on your credit card statement or simply look them up online.

Resolving these issues over the phone can be difficult sometimes because it is not always easy to get access to upper level managers who can make decisions, especially when your situation calls for a decision that is not a typical or standard resolution.

Also, some merchants will simply blow you off and make it virtually impossible to resolve anything. Finally, it is not always easy to show proof of the contents of a phone call and recording phone calls is not always permitted, so it is often difficult to prove an accurate record of the phone call.

You could also try to resolve things via email. However, it can be difficult to track down the email addresses for the managers that you need to reach (though there are ways to do this).

The good thing about email is you will have everything documented and this can come in handy later on when and if you need to supply documentation. The trick is finding the correct email addresses to send your email to.

Certified letter

If you are dealing with a substantial amount of money related to your transaction, then you might also consider sending a certified letter.

A certified letter gives you proof that the other side has received your correspondence. It does cost a little bit of money (it’s under five bucks) to send a certified letter but it gives you the necessary documentation that you might need later on.

Sending these letters also generally shows the merchant that you mean business when It comes to resolving your dispute and that you might resort to legal measures in the future.

Demand letter

A demand letter is a letter that you send out to a party when you are informing them that you’re planning on seeking legal action if they do not properly act to resolve the dispute. These are most effective when they are written by an attorney on a law firm’s letterhead and contain some type of legal “substance.”

With these letters you are essentially threatening to resort to legal measures to resolve the dispute if they are not willing to comply with your requests or demands.

As an attorney, this was always my go-to method for getting things done. Sending in a demand letter often got the other side to act promptly or at the very least got the conversation going, especially when I gave them a deadline to respond.

But not everybody has access to attorneys to write them legal demand letters and they may not feel comfortable drafting their own, so this route may not be practical for a lot of people.

Once you have attempted to resolve the issue with the merchant and it is clear that they are not going to work with you, then it is time to consider initiating a chargeback. Make sure that you have documented all of your attempts to communicate with them and any responses that they have given back.

Tip: Check out the free app WalletFlo so that you can optimize your credit card spend by seeing the best card to use! You can also track credits, annual fees, and get notifications when you’re eligible for the best cards!

What type of dispute are you filing?

Once you have tried to resolve things with the merchant unsuccessfully then you want to consider disputing the charge. You’ll first want to find out which type of purchase you’re trying to dispute: is it a billing mistake or are you disputing the quality of the goods or services.

Billing mistake

A billing mistake would be like getting charged two times for the same purchase or being charged for a canceled transaction. If you plan on filing one of these, you must submit a dispute within 60 days of the error first appearing on your statement.

If you contact Chase after 60 days, your options may be limited but Chase might still be able to assist you.

Goods or services

If you’re dissatisfied with the goods or services that you’ve purchased with your credit card, and you have tried in good faith to correct the issue with the merchant, you may have the right not to pay the remaining amount due on the purchases.

There are specific guidelines for disputing a transaction for goods and services though.

- The purchase must have been made in your home state or within 100 miles of your current mailing address, and the purchase price must have been more than $50. Chase considers any purchase made online or over the phone with a U.S. company to be from your home state.

- (Note: Neither of these is necessary if your purchase was based on an advertisement Chase mailed to you, or if Chase owns the company that sold you the goods or services.)

- You must have used your credit card for the purchase. Purchases made with cash advances from an ATM or with a check that accesses your credit card account do not qualify.

- You must not yet have fully paid for the purchase.

- If you are dissatisfied with goods or services on a purchase that does not meet the criteria above, you may still contact us to discuss other options.

Process to dispute a Chase charge

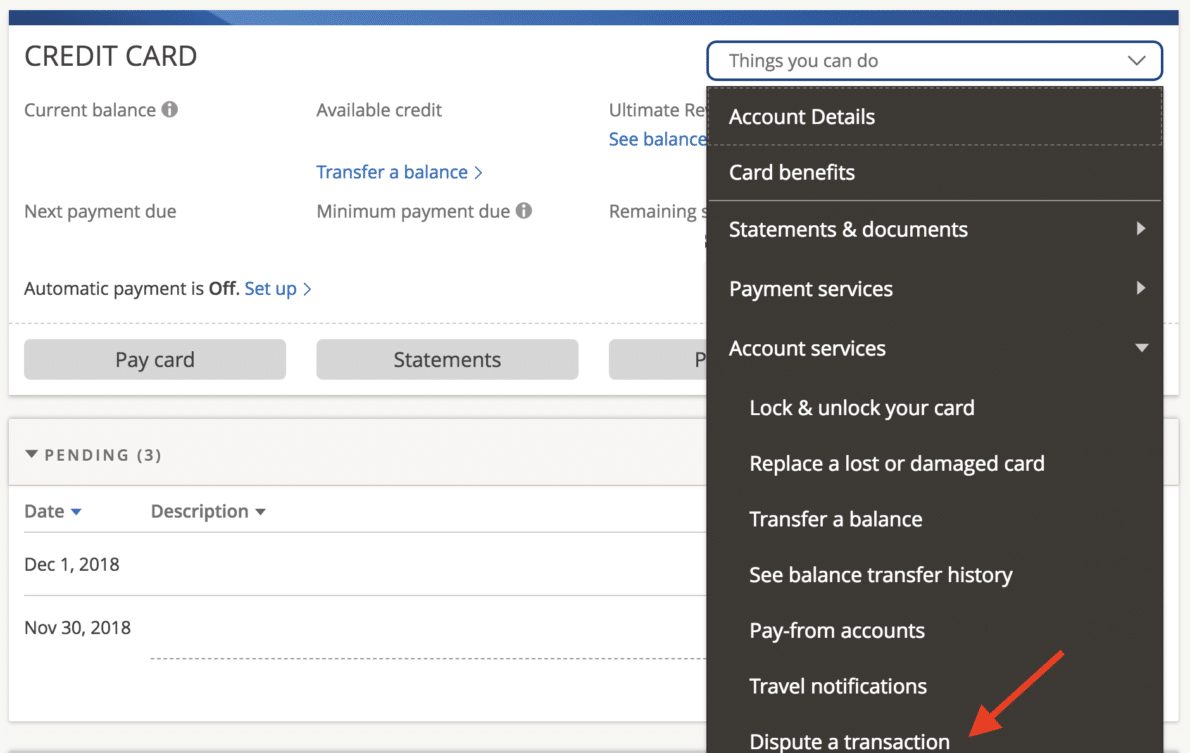

To do this simply log into your Chase account and then click on “Things you can do” and you will see “Dispute a transaction.”

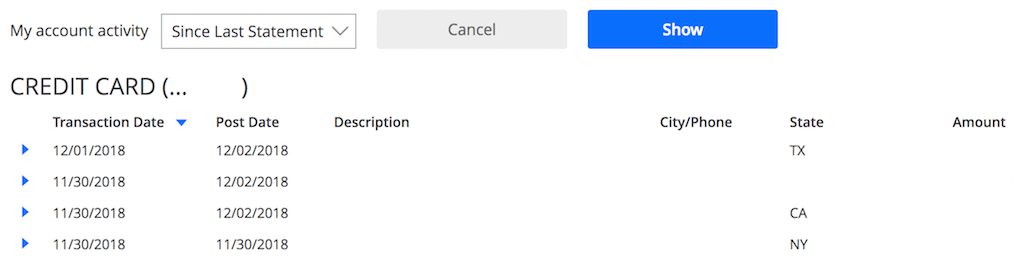

From there you will be able to review your prior transactions for that credit card:

Once you select a charge, you’ll then click “Dispute Transaction” where you’ll eventually be asked to choose from several fields that apply to your situation. These include the following.

- I’ve been charged twice for the same transaction.

- I don’t recognize this charge.

- I’m expecting a credit.

- I’ve been charged for a canceled transaction.

- I haven’t received service/merchandise.

- I received time/date sensitive service/merchandise too late.

- I’ve been overcharged.

- I’m dissatisfied with the quality of service or merchandise.

- I paid for the service/merchandise by other means.

- I never authorized this charge.

Supporting documentation

Sometimes Chase will request you to supply additional documentation. If you are dealing with an expensive transaction or a complaint of goods or services, there is a good chance that you will need to submit some documents.

For this reason, you want to make sure that you hold on to all of your related receipts. For example, it is not uncommon for rental car companies to charge you for gas when you have already filled up your rental vehicle. So in that case you would want to retain your receipt from whenever you filled up the car just in case.

It is also a good idea to take photos of any products if the product is at issue or the results of the service were subpar. Make sure you have all of your dates and times noted as well.

After you submit your claim, Chase will likely reach out and contact the merchant to investigate the issue.

If the specialist assigned to your dispute receives enough information to proceed, a temporary credit can be immediately applied to your account.

For credit card disputes, you will not be charged interest on the purchase during the dispute process. If the disputed amount is determined to be valid, Chase may re-bill you for the disputed amount, applicable fees and interest.

Chase states that they can settle most disputes in 30 to 60 days, but others may take longer.

Dealing with Chase

Unfortunately, Chase does not have the best reputation for being consumer friendly when it comes to dealing with these chargeback situations. Other issuers, such as American Express, are known for being very consumer friendly and easier to deal with.

So you should know that you might have a protracted battle ahead of you when dealing with getting your Charge disputed, depending on the complexity of the transaction.

Final word

Disputing a charge with Chase is not always the easiest thing to do because the processing time can be very long and Chase does not always side with consumers as much as some other issuers do. But if you do a good job of maintaining your records and follow the steps for processing your dispute, you shouldn’t be caught off guard by any surprises.

Daniel Gillaspia is the Founder of UponArriving.com and the credit card app, WalletFlo. He is a former attorney turned travel expert covering destinations along with TSA, airline, and hotel policies. Since 2014, his content has been featured in publications such as National Geographic, Smithsonian Magazine, and CNBC. Read my bio.

Hi Daniel,

I found your article very helpful. I recently went to Mexico for my bachelorette party and when I arrived the hotel stated they never received payment and demanded I pay again. I’ve tried to settle with the merchant but they just keep saying they don’t have the money. I opened a dispute with chase and submitted tons of evidence and lost the dispute. Any recommendations of how I should proceed next?

wow! this just happened to me too!

Thank you