The shopping cart trick is one of the most popular methods for getting approved for credit cards without a hard pull. It’s thus a very popular trick for people with low credit score and other people looking to get credit without hurting their credit score too much.

This article will show you how the shopping cart trick works, a list of stores you should try it at, and the steps you need to take to increase your odds of it working for you.

l’ll also explain some of the pros and cons of the shopping cart trick (like how it can both help and damage your credit score).

Interested in finding out the top travel credit cards for this month? Click here to check them out!

Table of Contents

What is the shopping cart trick?

The shopping cart trick is a way to get approved for credit cards without incurring a hard pull on your credit.

It’s a great method for establishing a credit profile and for getting approved for a credit card when you have a low score or can’t afford the hard pull.

December 2019 update: There are some reports here, here, and here of the Shopping Cart Trick still working for people. It’s definitely not as common as it once was but it seems you might still have a shot at some stores like possibly Overstock. My advice would be to check the MyFico forums and see the linked threads above for potential stores.

Tip: Use the free app WalletFlo to help you travel the world for free by finding the best travel credit cards and promotions!

Does the shopping cart trick still work?

As of December 2018, many data points are suggesting the shopping cart is dying out so proceed with caution. Approvals are still happening but hard pulls are becoming increasingly common (even when only the last four SSN digits are given). *SEE UPDATE ABOVE*

It’s a good idea to check on recent data points in comments, forums, etc. before trying out this method with a specific store.

Also, keep in mind two things.

One, the shopping cart trick does not work for everybody. I would give it a try at a handful of stores before I give up. If you can’t get the offer to pull up, then maybe try it again a couple of months down the line.

Second, the stores that it works for can change from time to time and some could result in a hard pull.

Preparing for the shopping cart trick

Before you try out the shopping cart trick you need to take care of a few things to make sure that you’ll stand a good chance of getting an offer.

Turn off pop-up blocker

If you don’t turn off your pop-up blocker or ad-blocker, you won’t be able to view the pre-approval offers.

So be sure that you do this.

If you already are running a pop-up blocker you may not be running it in a private browser or Google Incognito so you can just pull up a private browser if you don’t want to worry about disabling and enabling your ad blocker.

Opt-in to credit card offers

You absolutely must opt-in to credit offers to get this trick to work.

If you don’t then you will likely not ever receive a pre-approval offer.

If you need to change your opt-in status you do that here.

How to do the Shopping Cart Trick

There are several steps that you need to follow in order to get the shopping cart trick to work properly.

Follow the steps below very careful to ensure that the trick works for you.

Clear your browser history, cookies/cache

Before trying out the shopping cart trick you need to clear out your browser’s history along with the cookies/cache.

If you’re using Chrome for your browser you can just open up a an Incognito browser window.

Create an account

Next, you need to navigate to the website’s store that you want the credit card and you need to create a new account.

Be sure to use the same contact information (email, address, phone, etc.) that you would find on your credit report.

Some people forget to put in their middle names or middle initials and this can be a problem so be sure you enter the name exactly as it is found on your credit reports.

Another common problem is when an address is abbreviated in one profile and not in another. So if you input “Lane” in your address on your account for the store, make sure that your credit report doesn’t have your street listed as “Ln.”

Note: You should also try this without creating an account if the trick is not working. Sometimes checking out as a guest will work.

Add products to your shopping cart

You want to add items in your shopping cart to get this to work. You can try to add different amount of product to try to get the trick to work. Many will use $50 increments starting with $50 and then working their way up.

Some believe that there is a correlation between the price of items in your cart and the credit limit that you receive. So if you’re hoping for a high credit limit, consider adding a lot of products to your check out card and then just working your way down.

Checkout

Next, you’ll want to advance to the checkout stage and input all of your billing details (avoid autofill from putting in your details).

Make sure that you do not check out and purchase the items.

Wait

Now it’s time to wait for a pre-approval pop-up to appear.

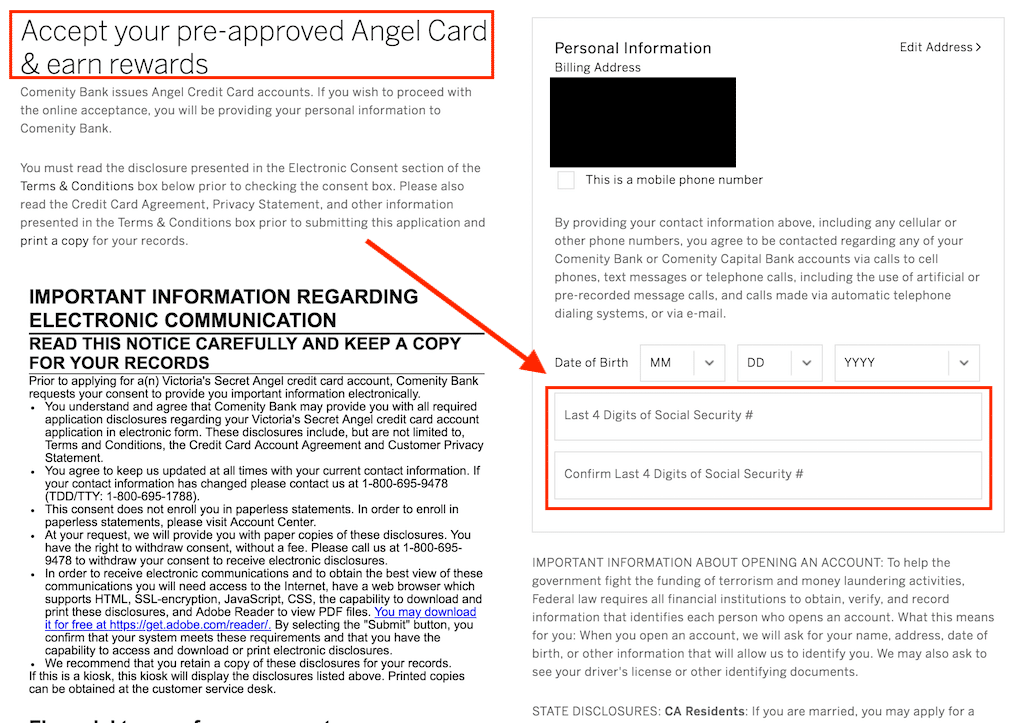

This is key: if the pop-up requests you to put your last four digits of your social security number into the pop-up then the shopping cart trip has probably worked.

However, if it asks for your full social security number then the trick is likely not working and your application will probably result in a hard pull.

Below is a pre-approved offer I pulled up from the Victoria’s Secret website (it was an experiment — I swear) while checking out as a guest. I had $366 worth of items in my cart and got pre-approved for a credit limit of $750.

Getting the pre-approval offer to show up isn’t the hardest part though. It’s getting the card without the hard pull that truly complete the trick. Sometimes the hard pulls can take a few days to show up so be on the lookout for them after you apply for a couple of days.

Can you do the shopping cart trick on mobile?

Yes, people have had success with Androids and iPhones pulling up the shopping cart trick pop-ups on mobile.

Just make sure you’re visiting the full “desktop” site and not the mobile site.

Shopping Cart Trick stores list

There are many stores that you can use (or at least attempt to use) the shopping cart trick for.

But the most common credit cards that work for the shopping cart trick are many of the Comenity credit cards. One credit card that seems to work very often is the Victoria’s Secret credit card and another very popular to try is the Wal-Mart credit card.

Keep in mind that some of the stores below might result in hard pulls — it’s hard to ever know 100% for sure that you won’t get a hard pull.

Comenity Store Cards

- Abercrombie & Fitch

- American Home

- Ann Taylor

- Bath & Body Works

- Big Lots

- Brylane Home

- Buckle

- Children’s Place

- Coldwater Creek

- Eddie Bauer

- Express

- Full Beauty

- Gamestop

- HSN

- Jared

- J.Crew

- Jessica London

- JJill

- King Size Direct

- Loft

- Motorola

- MyPoints

- New York & Company

- One Stop Plus

- Overstock

- PacSun

- Romans

- Sportsman Guide (watch out for hard inquiry)

- Total Rewards

- Venus

- Victorias Secret (very popular card to try)

- Wayfair

- Zales

Synchrony Store Cards

Wells Fargo Store Cards

The shopping cart does not work for:

If you apply for one of the cards below, you will likely receive a hard pull — don’t expect the shopping cart trick to work.

- Amazon

- Kohls

- PayPal

- Target

How many times can you do the shopping cart trick?

You can do the shopping cart trick multiple times and many people have done it many times in the past. Sometimes within the same month or week.

However, your account can get shut down if you do it too much.

Also, if banks see you opening up a lot of accounts in a short amount of time, that’s going to look bad and your credit score will take a hit as well.

So play it safe and don’t get too aggressive with your shopping cart tricks.

Why do people do the shopping cart trick?

The shopping cart trick is very popular because it can help you reduce damage to your credit report and get approved for cards even when you have a bad credit score.

I’ll walk you through some credit score basics as a refresher and then talk about the pros and cons of the shopping cart method.

Credit score basics

Knowing the basics of how your credit score works will help you understand how the shopping cart trick could both help and hinder your credit score.

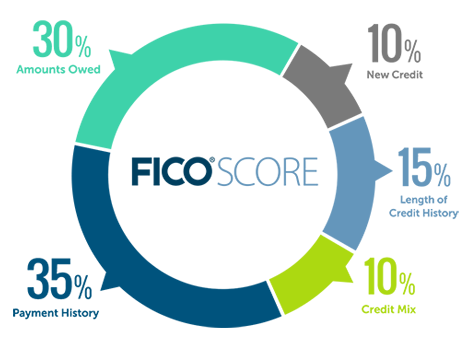

Your FICO credit score is determined in the following way:

- Payment History (35%)

- Utilization (30%)

- Credit History (15%)

- New Credit (10%)

- Mixed Credit (10%)

Payment History (35%)

Payment history is the #1 factor for determining your credit score.

Late payments will stay on your credit report for 7 years, although some bankruptcies will remain on your report for up to ten years!

Luckily, the negative effect of late payments and other negatives begins to lessen as more times passes.

How much a late payment affects your credit score depends on a mix of factors, including:

- How late they were and the number of past due items listed on a credit report

- The amount of money still owed on delinquent accounts or collection items

- How much time has passed since any delinquencies, adverse public records, or collection items

Utilization (30%)

Utilization is your credit to debt ratio.

to find this, divide the amount of debt you have by your total credit limit. So for example, if you have a $10,000 total credit limit and owe $5,000 in debt, then your utilization is at 50%.

If you have low overall credit limits then the shopping cart trick can benefit this category a lot.

Credit History (15%)

The credit history category consists of the of the following factors:

- Longest opened account

- Average age of account

- Time since newest account

- Time since each account was last used

The most important of these factors is the age of the longest opened account while average age of accounts is second.

You need to be mindful about your average age of accounts because that can be affected by opening up too many store credit cards.

New Credit (10%)

This category is most known for its effect felt from hard inquiries.

Hard inquiries result when your credit is pulled for review by lenders and certain other institutions and they differ from soft inquiries in the latter don’t affect your credit score.

Other factors besides hard inquiries in the new credit category are:

- How many new accounts you have

- How long it’s been since you opened your last account

This is another major factor that the shopping cart trick can impact, as discussed below.

Mixed Credit (10%)

This category evaluates your overall “mix” of credit lines.

So for example, it wants to see if you have a diverse range of credit consisting of different types of credit lines like student loans, auto loans, home loans, credit cards, etc.

Tip: Use the free app WalletFlo to help you travel the world for free by finding the best travel credit cards and promotions!

Benefits of the shopping cart trick

Here are the major benefits of the shopping cart trick.

Get approved for cards with low credit scores

This is very important for people who have no credit or payment history or very low credit scores who can’t get approved for many credit cards. It gives them a shot at actually opening up a new credit card and therefore benefiting their credit score.

If you have no credit history then the shopping cart trick can be one of the best ways to improve your credit score. Just continue to make your monthly payments on time and eventually you will start to establish a credit profile.

Decrease utilization

It also can decrease your utilization which will improve your credit score. For people who have large balances on credit cards, this can help lower their utilization a little.

Just remember that many of these credit limits are not going to be very high so the benefit to your credit to debt ratio is going to be low.

You can always try to get a credit limit increase once you’ve had your card form 6 to 12 months. Many times, you can get a credit limit increase without even incurring a hard pull.

Maintain a perfect score

A hard pull will usually lower your credit score between 2 to 5 five points, depending on your credit score. If your credit score is lower and your credit profile is very thin, you could receive an even bigger hit to your credit score.

But this trick could also be useful for someone who is trying to work their way up to getting the perfect credit score.

Drawbacks of the shopping cart trick

I’ve talked about how you can avoid the damage from a hard pull which is great for preserving your score and allowing to your credit report to be less blemished.

But these cards will still report to your personal credit report.

This means that they could lower the average age of accounts and also hit you with a new account which will lower your credit score. The impact tends the biggest when you don’t have a very established credit profile. So if this is your first credit card you might get a pretty big drop in your credit score.

The good news is that this drop will be temporary. Give it a few months and your score will probably be back where it needs to be.

Improving your credit score

Getting credit cards without credit pulls isn’t the only way to boost your credit score and it will only do so much.

Luckily there are a few ways that you can quickly boost your credit score.

Get a “starter” credit card

If you have a poor credit credit score, you’ll likely struggle to get approved for many credit cards.

However, there are many credit cards available for people with bad credit like store credit cards, such as the Zales credit card.

Get added as an authorized user

Adding yourself as an authorized user to a credit card can be a great way to raise your credit score immediately (relatively speaking).

Becoming an authorized user can improve your credit score by doing these things:

- 1) Lowering your credit card utilization

- 2) Improving payment history

- 3) Increasing the average age of accounts

- 4) Diversifying your credit (this factor plays a very limited role).

Balance transfer to business credit card

The strategy here is to transfer a credit card balance to a business card because most business card balances to not report to your personal credit report. So while you’re still responsible for paying the balance, it’s almost like that balance doesn’t exist for purposes of your credit report

Consolidate your revolving credit into an installment loan

Did you know that installment loans are not factored in to your credit score?

This means that if you can transfer over your debt from a credit card to a bank installment loan then you can immediately lower your utilization.

I’ve seen people raise their credit scores by 100 points overnight with this method by bringing maxed-out credit utilization down to 0%.

Goodwill letters

Your payment history makes up 35% of your score and is therefore the most important factor in your credit report, so it’s vital to take care of this factor.

If late payments or delinquencies are holding you back, then trying a goodwill letter might be one of the best ways to quickly improve your credit score.

They don’t take much time to put together and there’s usually very minimal risk with giving them a try so it’s always worth it to try your luck with a goodwill letter.

Get errors removed

An Federal Trade Commission (FTC) report found that 21 percent of a representative group of US consumers found a “confirmed material error” in one of the credit reports issued by the big three credit bureaus.

So there’s a 20% chance or better that you have an error on your credit report that does not belong and that is damaging your credit score.

Consider performing an audit on your credit score

You can read more about all of these methods here.

Final word

The shopping cart trick is still alive and well in 2018. For the time being, you can pick up credit cards with no credit pull and help build up your credit profile or just add some credit to your profile without incurring a hard pull.

Just keep in mind both the pros and cons of the shopping cart trick and your credit score won’t take a major hit.

Daniel Gillaspia is the Founder of UponArriving.com and the credit card app, WalletFlo. He is a former attorney turned travel expert covering destinations along with TSA, airline, and hotel policies. Since 2014, his content has been featured in publications such as National Geographic, Smithsonian Magazine, and CNBC. Read my bio.

I learned very recently (11/2020) that Credit Card Utilization DOES NOT get factored into your FICO score if you are on someone else’s card as an authorized user…only the payment history does. I have a membership through MYFICO.com which gives me my FICO score for all three bureaus. I am an authorized user on two credit cards. The payment history was factored into my FICO score but it showed nothing on the utilization. I hit the little question Mark And it said the utilization rate does not get factored in With the cards that you are an authorized user on. I wish I could add a picture here so that I could attach the screenshot to this post. I was devastated to learn this since I always thought that Being added as an authorized user what affects two things; utilization and payment history. That said…They do use the information for your payment history