A lot of people (including myself) rely on Credit Karma to monitor their credit score to make sure everything stays up to par. It’s a very easy and free to use tool so it is very understandable that it is one of the most popular ways to keep track of your credit score. But exactly how accurate is Credit Karma?

In this article, I will talk about whether or not Credit Karma is accurate and some of its potential shortcomings as well as its strengths. I’ll also show you how to find a more accurate credit score that can better predict your credit approval odds.

Table of Contents

How accurate is Credit Karma?

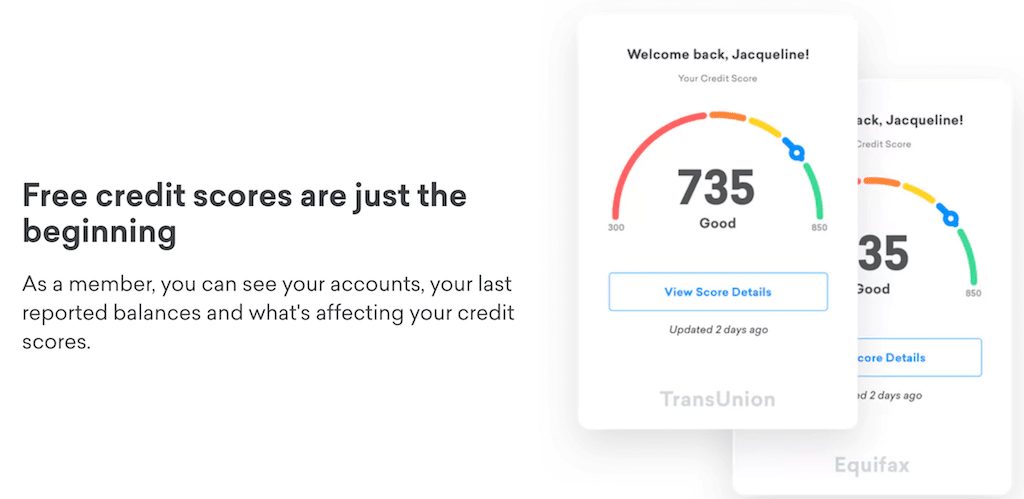

Credit Karma is an accurate way to check your Vantage credit score with TransUnion and Equifax. However, there are a few issues with this.

One issue is that most lenders utilize the FICO model and Credit Karma uses the VantageScore Model which means that the scoring system is different from most lenders. So it is not so much that Credit Karma is inaccurate; it is just that it utilizes a model that most lenders do not use.

The second issue is that Credit Karma does not provide you with an Experian score. Many lenders, including many credit card issuers, like to pull your credit score from Experian.

If your Experian credit report has different marks on it compared to your Equifax or TransUnion report, then there could be a large discrepancy between your Credit Karma score and what the credit card issuer sees. You can read on more here about which credit card issuers pull from which credit bureaus.

Tip: Use WalletFlo for all your credit card needs. It’s free and will help you optimize your rewards and savings!

What is the VantageScore Model?

The VantageScore Model was originally developed in 2006 and the VantageScore Model 3.0 debuted back in 2013. There is currently a 4.0 model as well but it has not been as widely adopted as it has only been out since 2017. VantageScore Model 3.0 is used for other credit services like Credit Wise, Chase Journey, etc.

The VantageScore Model Credit Karma uses is pretty similar to the FICO model but it has some key differences. It uses the same FICO range of 300 to 850 for the score and stresses many of the same factors as FICO — it just gives them different weight and has some slightly different criteria for calculating them.

Here are the 3.0 factors according to Credit Karma:

- Payment history (about 40%)

- Age and type of credit (about 21%)

- Credit utilization (about 20%)

- Balances (about 11%)

- Recent credit (about 5%)

- Available credit (about 3%)

Here are the factors for the FICO model.

- Payment History (35%)

- Utilization (30%)

- Credit History (15%)

- New Credit (10%)

- Mixed Credit (10%)

Payment history

Just like the FICO model, payment history is the number one factor.

It makes sense the number one concern for a credit score is to determine how big of a credit risk you are. Your track record with paying your bills on time is the number one indicator for that so it is no surprise that it is the most influential factor for both models.

However, payment history appears to be even more important for the VantageScore Model since it weighs in at 40% versus 35% for FICO.

The 3.0 model will not penalize you for collections which have been paid which is a departure from some FICO models. That right there can make a huge difference for people who have multiple items in collections and have paid them off.

FICO models will only allow you to have payment history if you have six months of established history. Meanwhile, you can have payment history under the Vantage model with only one month of payment history. This trips a lot of people up sometimes because they can pull up a credit score with Credit Karma but they still are not able to pull up a FICO score.

Age and type of credit

This is different from the FICO model because account history and the types of credit are two of the three least important factors for FICO. One of the big differences for the VantageScore Model is that it does not consider closed accounts when determining the age of your accounts. FICO will continue to count your closed accounts until 10 years after they are closed.

So your average age of accounts will often be significantly lower with the VantageScore Model. This is why people like me who have opened up and closed a lot of cards have a significantly lower VantageScore Model Score than FICO — the average age of our accounts is significantly lower and it carries more weight.

Credit utilization and balances

Credit utilization is only about 20% of your Vantage score. Meanwhile, it is the second most important factor for your FICO score. So if you have maxed out cards or cards with high balances it should hurt you less for your Credit Karma score but be much more impactful for your FICO score.

It is a little confusing to me what the difference is between utilization and balances, though. Credit Karma states, “[balances] refers to the total amount of recently reported balances (current and delinquent) on your credit accounts.”

So to me it sounds very similar to utilization. I think that this could be more focused on individual utilization, which would be the individual balances on each of your accounts. Regardless, it sounds like it is equally important to keep your balances down for both of these types of credit scores.

Related: Should You Pay off Your Credit Card Balance Each Month?

Recent credit

Your recent credit is going to look at new accounts just opened and also new inquiries. One big difference here is that the Vantage models will combine related inquiries within a 14 day window. Meanwhile, newer FICO versions count multiple credit inquiries of the same type within a 45-day period as a single inquiry.

Therefore, if it took you 3 1/2 weeks weeks to find an auto loan and you had multiple inquiries within those weeks, that could have had a bigger impact on your Vantage score versus your FICO score.

Available credit

Available credit is the least important factor for the 3.0 model. According to a VantageScore® Solutions report, prime consumers keep $20,000 to $22,000 worth of credit they don’t use. At only about 3% of your score, this factor is almost completely a non-factor.

Is Credit Karma really that inaccurate?

The difference between your FICO Scores scores and your Credit Karma scores can be quite extreme. There are reports of people with Credit Karma scores over 700 with both bureaus but with FICO scores in the lower 600s.

Other times, the opposite might be true. Your Credit Karma score could be much lower than your FICO score. It all depends on the make up of your specific credit profile.

Should I even bother with the Credit Karma score?

Since most major lenders utilize the FICO model, you need to be very cautious about relying solely on your Credit Karma score. As I have shown, in some instances, this score can be really different from your FICO score like when you only have a couple of months of credit history or when you have closed a lot of credit card accounts.

Sometimes a lender might have a hard cut off for approvals or for certain interest rates. For example, if your score is below 700 your interest rate could go up another 1% or 2%. Or if your score is below 650 you might not be able to get approved for a certain loan or card.

In those cases, when you were dealing with hard cutoffs, it becomes very important that you get a truly accurate and up-to-date score. This is especially true if you are dealing with a large sum of money like in the case of a mortgage.

In those situations you would want to stray away from Credit Karma and do what you can to obtain an official FICO score. It will also benefit you to try to figure out exactly which credit score model your lender uses, since there are many different versions of FICO score.

And some point you might actually run into a lender that uses the Vantage score model (many lenders do use it). If they are pulling from Equifax for TransUnion then Credit Karma could be very useful for that lender.

Where can I get accurate FICO credit scores?

There are a few ways that you can get a FICO score.

Many find it easy to sign-up for Experian.com and utilize that to get their FICO score (they offer a free 30-day trial membership). If you are just in it for the free score, make sure that you cancel your membership.

Sometimes MyFICO offers a free trial so be on the lookout for that.

You can also get one free credit report from each of the three major credit bureaus (TransUnion, Equifax, and Experian) once every 12 months from annualcreditreport.com. But note that that is usually just the report (though I’ve been given the score once in the past before).

Many credit card issuers will now allow you to check your FICO score for free. So if you have a credit card account with any of the major issuers like Chase, American Express, Discover, Capital One or many others you should look into checking for a free score.

Credit Karma credit score simulator

Credit Karma has a special tool that allows you to see what might happen to your credit score if you take certain actions. For example, you can predict the effect on your credit score if you open up a new loan or credit card. I have played around with this tool in the past, and found it to be somewhat accurate but nothing that I would definitively rely on.

The biggest shortcoming of this simulator is that it only allows you to tweak one element at a time. In reality, when you make a change on your credit report, several factors are probably going to be affected and that can make a huge difference.

So feel free to play around with the tool but keep in mind that the outcome of your changes could be very different.

So is Credit Karma ever useful?

I think that Credit Karma is still very useful for a lot of people and here is why.

Easy to use

First of all, it is just a very easy to use app and it is a great way to keep track of your Equifax and TransUnion credit reports. If you’re concerned with trying to see how many accounts you have open or how many recent inquiries you have had, then Credit Karma can be extremely useful.

For example, you might want to calculate your 5/24 status and Credit Karma can be a great way to do that (although I’d probably use annualcreditreport.com).

Insights

Credit Karma offers insights when you are reviewing your credit report. These insights will tell you what factors are affecting your score the most, and whether or not those things are positive or negative.

If you already are well-versed in credit reports, then these insights really won’t tell you anything that you don’t already know. But for people who are still learning how credit scores work, these insights can be very helpful.

The insights can also tell you things like if you are paying too much for your interest rates. I have not relied on these type of insights in the past so I am not sure how helpful or accurate they are.

Credit monitoring

It also can be very handy when you are just trying to monitor your credit report. You should get notifications or emails whenever a new account is opened or an account is closed. And you should also get notified in the event you ever have a late payment or some other negative mark on your credit report.

Sometimes Credit Karma can get a little annoying when they send me notifications “reminding” me that my payment history is still 100%. These emails tend to give me mini heart attacks because all I see is a notification about my payment history and I could do without those.

Disputing items

You can also use Credit Karma to dispute items on your credit report. So if you are in the process of trying to clean up your credit report, then Credit Karma could actually be a good way to start. Typically, I like to dispute the items directly with the credit bureau. However, it is convenient to utilize a third-party like Credit Karma for a lot of people.

And even if you don’t utilize Credit Karma to initiate the dispute, it can still be a very useful way to get organized when preparing to dispute an item.

Debt repayment calculator

You can utilize the debt repayment calculator to figure out how long it will take you to pay off some of your bills.

Unclaimed money

Credit Karma also has a feature that allows you to view if you have any unclaimed money. You might be entitled to collect a couple of hundred bucks and not even realize it.

Final word

Credit Karma is not the most accurate tool that you want to use for most lenders since they use a different scoring model (FICO). Generally speaking, Credit Karma can give you a good idea of where your credit score stands. However, if you have had a lot of activity such as multiple closed accounts, the score that it gives you will often be skewed and much lower than what your FICO score is.

With that said, I still think that it is a great tool to use that can help you monitor your credit and it is free so there really is no hurt in giving it a shot.

Daniel Gillaspia is the Founder of UponArriving.com and the credit card app, WalletFlo. He is a former attorney turned travel expert covering destinations along with TSA, airline, and hotel policies. Since 2014, his content has been featured in publications such as National Geographic, Smithsonian Magazine, and CNBC. Read my bio.

I find Credit Karma to be very inaccurate. I bought a guitar on Sept 29, 2020 for $5,000.00. I used my credit card. I paid this off with a one time payment to the bank on October 6, 2020. My credit dropped something like 73 points immediately. It is now Nov 8, and no change. Credit Karma still shows me owing $5,000.00. Last time this happened, the last time I used my card, it went on for 6 months after it was paid off.

I was super excited with credit Karma until the last few months, now it seems that it is only interested in giving inaccurate credit scores and excuses. My credit dropped immediately by 30 plus points with a loan in Sept of $5000. I paid this loan off in full on 23 Dec and had a 0 balance and now on the 16th of Jan a new balance of $3025 has shown up and my credit score has dropped again by 15 points. What happened, a dispute would take 30 plus days while my credit suffers. Credit Karma clean up this bad practice…

my credit score dropped 24 points because of a 8,000 charge on a credit card.I have 40 year credit history of never missing a payment or being late. I have a 35,000 dollar monthly in come and a networth of 6,000,000 to 7,000,000. I could pay this charge in less than 1 weeks of salary. My checking account has a 6 figure balance. It is easy to see you do not have the information to give someone an accurate credit score.